1. The Headline No One in Affiliate Marketing Should Miss

In FY2026, two African mobile operators each processed more than half a trillion dollars in transaction value through their mobile money platforms.

- Vodacom Group (M-Pesa, MoMo across South Africa, Tanzania, DRC, Mozambique, Lesotho, plus Safaricom): $525.6 billion processed, 103 million financial services customers, financial services revenue up 19.6% to R16.8 billion.

- MTN Group MoMo (across 16 African markets): $500.3 billion processed, 69.5 million monthly active users, transaction volume up 14.9% to 23.3 billion individual transactions.

Together they processed more than $1 trillion in a single year. That is more than the GDP of most countries they operate in.

It is also far more than what their core voice and data business generates. Mobile operators are no longer telecoms. They are the dominant retail banks of Africa and large parts of Asia. They just happen to also sell SIM cards.

For affiliate marketers — especially those used to thinking of telcos as the people who run DCB and mVAS offers — this is a much bigger story than another quarterly results headline. It is a structural change that opens an entirely new vertical.

2. The Numbers Across Three Regions

This shift is not isolated to one operator or one country.

Africa — telco-led mobile money dominates

| Operator | Active users | 2025 transaction value | Growth |

|---|---|---|---|

| Vodacom (M-Pesa, MoMo) | 103M | $525.6B | +16.6% |

| MTN MoMo | 69.5M MAU | $500.3B | +37.6% in const. currency |

| Airtel Africa Money | 54.1M | ~$215B annualized | +21.3% users |

The “advanced services” — lending, savings, insurance, merchant payments — are the fastest-growing piece. At MTN, advanced services are already 34.1% of MoMo revenue (excluding airtime), up 4.2 percentage points year-on-year. At Vodacom M-Pesa, “beyond core” services hit 46.4% of M-Pesa revenue in the International segment.

Translation: the era of mobile money as “phone-based P2P transfers” is over. These platforms are now real banking ecosystems.

Asia — telco-affiliated super-apps

| Wallet | Operator partner | Users | Annual transaction volume |

|---|---|---|---|

| GCash | Globe Telecom (Philippines) | ~94M | ₱3 trillion (~$52B) |

| bKash | Axiata / BRAC Bank (Bangladesh) | 82M+ | Tk200B in remittances alone |

| DANA | Indosat Ooredoo Hutchison (Indonesia) | Top-4 nationally | One of the dominant e-wallets |

GCash alone now accounts for 41% of e-commerce transaction value and 29% of POS payments in the Philippines.

US and Europe — telcos as bank distribution channels

The shift in the West looks different. Telcos there cannot get banking licenses easily, so they partner.

- Verizon + Openbank (Santander) launched in April 2026: Verizon-branded high-yield savings accounts inside the Verizon app. Rates 10× the national average. Bill credits up to $180 per year if customers maintain a minimum balance. Verizon owns the relationship, Santander provides the regulated infrastructure.

- Similar pattern with Apple + Goldman Sachs, Amazon + JPMorgan Chase, Walmart + Green Dot.

In emerging markets the operator owns the wallet. In developed markets the operator becomes the storefront. Either way — the consumer’s primary banking relationship is increasingly with a brand that used to “just” sell connectivity.

3. Why Now

Three forces are converging:

1. Telcos have what banks want. They have 5.6 billion mobile subscribers globally, daily engagement (people unlock phones 50–100 times a day), KYC data from SIM registration, biometric capability via face/fingerprint, distribution through agent networks (Vodacom alone has 705,000+ M-Pesa merchants in International markets and 3.2M at Safaricom).

2. Banks lost the emerging-market customer years ago. In countries with low card penetration and limited bank-branch coverage, the bank-led financial inclusion story largely failed. Mobile money walked in and filled the gap. Now that population has graduated from P2P transfers to wanting loans, savings, insurance, and merchant payments — and they want it from the brand they already use ten times a day.

3. Connectivity revenue is structurally flat. Voice ARPU is in slow decline almost everywhere. Data ARPU is plateauing as customers hit “good enough” consumption. The only way for telcos to grow service revenue at double digits is to add adjacent services. Financial services delivers exactly that — Vodacom financial services grew 19.6%, more than 2× the rate of mobile service revenue.

These forces will not reverse. If anything, they will accelerate in 2027–2028 as more telcos copy the playbook.

4. What This Means for Affiliate Marketers

If you are an mVAS or DCB affiliate today, the temptation is to read this as a sidebar story — “interesting, but not my vertical.” That would be a mistake.

The wallet rails that handle $1 trillion a year on Africa and Asia are the same rails that bill many of your mVAS subscriptions, recharge airtime credit, and identify users via MSISDN. As telcos invest in wallets, the wallet often displaces DCB as the primary billing rail — and the offers running on top of it shift accordingly.

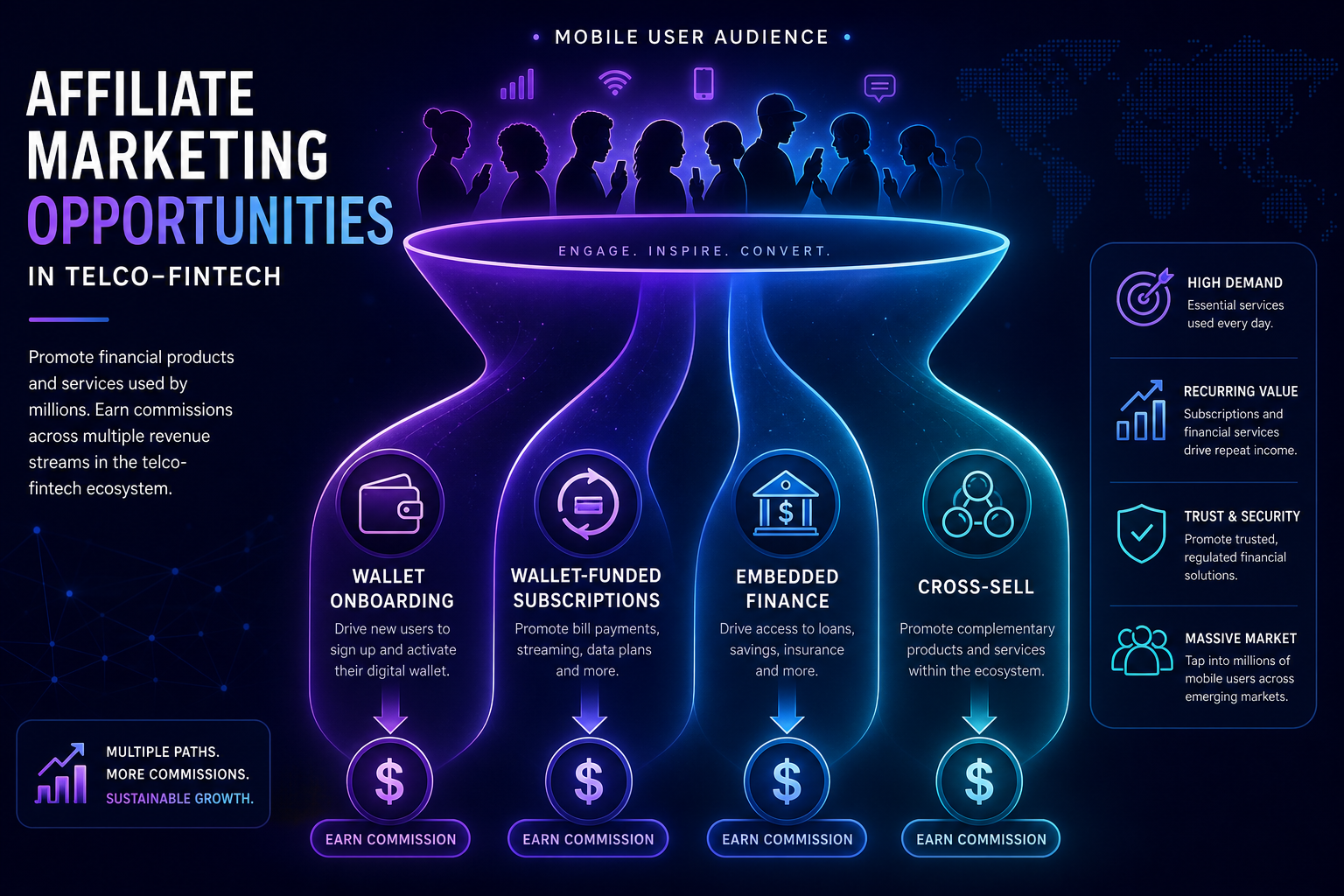

Four concrete affiliate opportunities to watch in 2026–2027:

Opportunity 1. Mobile wallet onboarding (pure CPA)

Major wallets actively pay for new verified user signups. GCash, bKash, MTN MoMo, Airtel Money, and Orange Money all have referral or partner programs. Payouts vary from a few dollars to double digits per verified KYC signup, depending on market and tier. For traffic sources targeting Tier-2/3 emerging-market audiences who are already smartphone users but not yet financially served, this is a clean CPL/CPA play with no recurring billing complexity.

Opportunity 2. Wallet-funded subscriptions (DCB evolution)

When a user funds a subscription from a wallet instead of from prepaid airtime, three things change:

- Billing success rates jump (wallet balances are larger and more stable than airtime balances)

- Fraud and chargeback rates drop (wallets have proper KYC)

- LTV per subscriber rises

Some mVAS advertisers in markets like Kenya, Ghana, Bangladesh, and the Philippines are already offering “subscribe with M-Pesa” or “pay with GCash” variants of their landing pages. CR is sometimes lower than 2-click DCB, but net EPC after retention is often higher. Worth A/B testing wherever the option exists.

Opportunity 3. Embedded finance offers (CPL / CPS)

This is the most underdeveloped opportunity. Telco-led lending, savings, and insurance products generate hot CPL leads when promoted to the right audience:

- “Get a loan in 60 seconds from MTN MoMo” — instant credit decision, no paperwork

- “Open a high-yield savings with Verizon + Openbank — earn $180/year in bill credits” — clear value prop, sticky once opened

- “Insurance bundle through your operator wallet” — micro-policies starting at $1/month, perfect for emerging-market audiences

Networks that have direct relationships with telco-fintech advertisers can start placing these offers now. Expect the inventory to expand rapidly.

Opportunity 4. Cross-sell within the mVAS user

If you already own a subscriber to an mVAS product on a given operator, that user is a warm lead for the operator’s wallet-based services. As more advertisers offer attribution windows that span verticals (entertainment → finance), affiliates who already control top-of-funnel mVAS traffic are best positioned to capture the second commission on the same user.

5. The Bigger Picture: Convergence, Not Disruption

This is not a story of fintech disrupting telecom. It is the opposite — telecom disrupting fintech in the markets where banking infrastructure was always thin.

For affiliate marketers, the implication is bigger than picking up a few new offer types. The whole funnel is changing:

- The payment rail is shifting from raw DCB toward wallet-funded transactions

- The user identity is shifting from MSISDN-as-anonymous-identifier to MSISDN-as-bank-customer with full KYC

- The product mix is expanding from “buy this digital subscription” to “buy this digital subscription / loan / insurance / savings — through the brand you already trust”

- The trust layer is improving — users transact more confidently when their telco wallet sits behind the purchase

That should make funnels cleaner, conversions more durable, and affiliate-to-advertiser relationships richer. It also means affiliates who learn this vertical early will have a multi-year head start over those who keep optimizing only what they did in 2024.

6. Bottom Line

- In FY2026 Vodacom and MTN each processed roughly half a trillion dollars through mobile money — more than $1 trillion combined.

- Asian telco-affiliated wallets (GCash, bKash, DANA) and Western telco-bank partnerships (Verizon + Openbank) repeat the same pattern in different ways.

- For affiliates this opens four new opportunities: wallet onboarding, wallet-funded subscriptions, embedded finance offers (lending / savings / insurance), and cross-sell within existing mVAS audiences.

- Networks and affiliates who start testing this inventory in 2026 will own the category in 2027.

- The trend is not about telcos doing finance as a side gig. It is about telcos becoming the primary financial brand for hundreds of millions of users — and that reshapes which offers convert and how.

Want to know which telco-fintech offers are already live across MTN MoMo, M-Pesa, Airtel Money, GCash, and bKash with our network? Sign up with Affiliate Dragons and our manager will walk you through the inventory and show you which GEOs are ready for your traffic right now.